The Risk Dashboard, based on Solvency II data, summarises the main risks and vulnerabilities in the European Union’s insurance sector through a set of risk indicators.

The data is based on financial stability and prudential reporting collected from insurance groups and solo insurance undertakings.

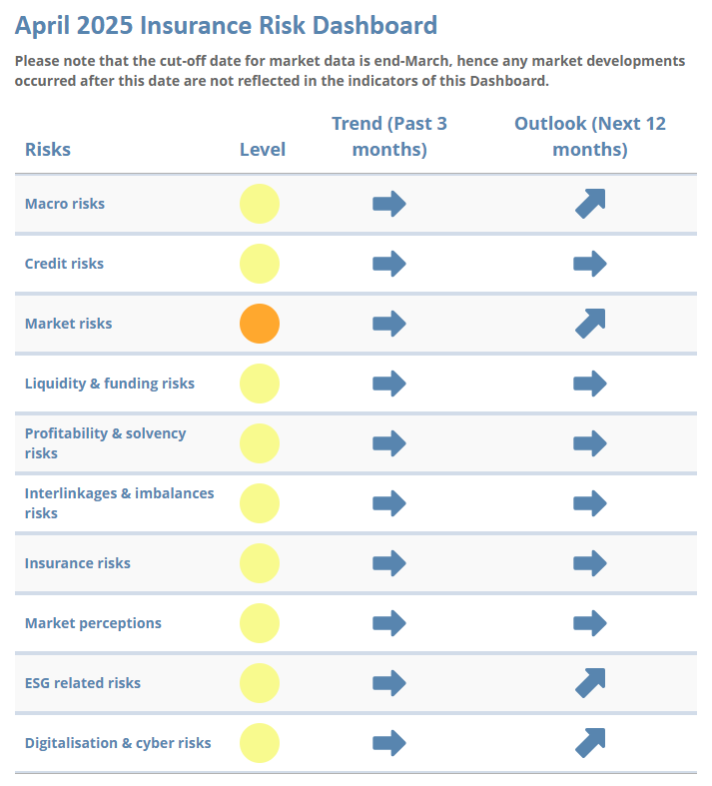

Insurance Risk Dashboard April 2025 (Q4-2024 Solvency II Data)

Key observations:

The April 2025 Insurance Risk Dashboard is based on Q4 2024 Solvency II data and Q1 2025 market data. The main findings show that risks in the European insurance sector are stable and overall at medium levels, with pockets of vulnerabilities stemming from ongoing market volatility related to high geopolitical uncertainty.

Global macroeconomic risks remain stable at a medium level, with a slight decrease in GDP growth and an increase in inflation forecasts. Looking ahead, geopolitical uncertainty and fragmentation may negatively impact the macroeconomic landscape.

Credit risks remained stable through March 2025, with minimal movement in spreads and only slight shifts in investment allocations. Portfolio quality stayed high despite a small rise in lower-rated assets. Early April saw a modest widening of spreads as financial market participants reassessed risk premiums.

Market risks remain elevated amid high volatility in bonds and equities, with a worsening risk outlook. Insurers slightly increased their bond exposures, while equity holdings held steady. Real estate values fell, but insurers’ exposures stayed limited. In April, the announcement of US tariffs triggered sharp market reactions. While markets have stabilised somewhat, further asset price corrections are likely in view of high policy uncertainty.

Liquidity risks stayed at a medium level. Cash holdings continued to be stable and cash flow positions stayed positive. Insurers’ liquid asset ratios slightly increased even as lapse rates remained elevated at the end of Q4 2024. On the derivative side, while the insurance sector has been resilient in addressing liquidity needs so far, effective liquidity management remains crucial to navigate potential new market shocks in the current environment.

Solvency and profitability risks held steady. Solvency ratios were robust in the last quarter of 2024, with slight shifts across different segments. Profitability showed mixed signals, with some return metrics improving while others fell. The non-life combined ratio was unchanged.

Risks stemming from financial interlinkages remained stable. Exposures to banks, reinsurers, and derivatives showed little change, and reinsurance cessions stayed consistent.

Insurance risks were also stable, with both life and non-life premium growth rising while loss ratios showed a slight decline.

Market sentiment remained at a medium risk level. Life insurers outperformed the market in March, though European insurance stocks were impacted negatively in April, mirroring broader market trends.

ESG risks were steady but with an intensifying outlook. Green bond exposures increased, while climate-sensitive assets dipped. In the current geopolitical context, shifting environmental agreements are creating additional challenges to achieving long-term sustainability objectives.

Cyber and digital risks stayed at a medium level, albeit with a rising outlook. Threat perceptions have increased, with geopolitical tensions remaining a key factor.

Go to the April 2025 Insurance Risk Dashboard

Note:

- The reference date for company data is Q4-2024 for quarterly indicators and 2023-YE for annual indicators. The cut-off date for most market indicators is the end of March 2025.

- The Level (color) corresponds to the level of risk as of the reference date, the Trend is displayed for the 3 months preceding the reference date and the Outlook is displayed for the 12 months after the reference date. The latter is based on the responses received from 23 national competent authorities (NCAs) and ranked according to the expected change in the materiality of each risk (substantial decrease, decrease, unchanged, increase and substantial increase).

Previous Dashboards

EIOPA's previous Insurance Risk Dashboards are available here.